Centralized vs. decentralized stablecoins

A stablecoin is a type of cryptocurrency that aims to have its value stabilized to another currency or asset. Most commonly, stablecoins are pegged to the U. S. Dollar, such as $USDT, $USDC, and $DAI.

A stablecoin is a type of cryptocurrency that aims to have its value stabilized to another currency or asset. Most commonly, stablecoins are pegged to the U. S. Dollar, such as $USDT, $USDC, and $DAI. Although there exist others pegged to gold or the Euro, these are less popular, and liquidity on the markets is less substantial. That is the reason why we will focus mostly on Dollar backed stablecoins.

Centralized Stablecoins

Centralized stablecoins are tokens that require trust in a third party to maintain their peg. Third parties are centralized entities that hold the stablecoin's collateral or reserve assets off-chain.

These types of stablecoins are, to date, the most popular and have the most liquidity in the market, with $USDT and $USDC taking the top spots when market capitalization is concerned.

The reason that they are more popular than decentralized stablecoins is that people at the moment are more confident knowing that their token is backed one-to-one in a bank. That is due to certain non-custodial stablecoins losing their peg in volatile market conditions.

Decentralized Stablecoins

Decentralized stablecoins are tokens that are autonomous and/or governed by a DAO (Decentralized Autonomous Organization) foundation and maintain their peg without the need of a centralized entity holding the reserve asset. Notable examples of decentralized stablecoins are Maker’s $DAI and the now-defunct Terra's $UST. However, both projects have used two different philosophies when it comes to how to secure their stablecoin.

Exogenous collateral.

Exogenous collateral is an asset that has other uses outside of maintaining a stablecoin peg. Meaning only a small portion of the entire supply is used to be collateral for the stablecoin.

This is the case with Maker Dao’s $DAI. Users place Ether in Maker’s vault to mint $DAI. If $DAI is trading for more than a dollar more, users will mint $DAI. This will flood the market with $DAI, which will return to its dollar value.

$DAI is also often referred to as a collateralized stablecoin.

Endogenous collateral.

Endogenous collateral is an asset that has little to no outside use aside from being collateral for a stablecoin.

This was the case with Terra. Terra users placed $LUNA as collateral to mint $UST. And $UST could be burned to mint $LUNA. However, the Terra ecosystem failed to maintain the peg of $UST.

This failure was due to $UST being under collateralized by $LUNA. Therefore there was not enough collateral to burn to maintain the $UST peg. This effect is commonly known as a “death spiral”. In the $LUNA case, once $UST reached a higher market capitalization than $LUNA, massive amounts of $LUNA tokens were created to collateralize $UST. That uncontrolled creation of tokens led to the devaluation of $LUNA. Once the “death spiral” started, there was no way to re-peg $UST.

Terra is a good example of an algorithmic stablecoin, where the collateral does not fully back the peg, and stability is maintained through game theory and stabilizing algorithms.

Decentralized Data Feeds

Decentralized or non-custodial stablecoins require data feeds of market prices to be able to maintain their peg. This data is not natively accessible on-chain. Here's where oracle networks like Chainlink come into play.

Oracles are entities that connect blockchains to the external world, as well as other blockchains, thereby enabling smart contracts to be executed based upon inputs and outputs from the real world. Using oracles non-custodial stablecoins can gain access to reliable data and maintain decentralization.

There would be no point in having a centralized data feed, as it would generate a single point of failure, and could be easily bribed or corrupted, undermining the decentralized nature of the stablecoin.

Custodial Stablecoins Controversy

If you have been in the crypto-verse for any amount of time, you probably know that trust in centralized entities such as banks is the antitheses of DeFi (Decentralized Finance) and cryptocurrency. That is the reason why decentralized stablecoins first emerged.

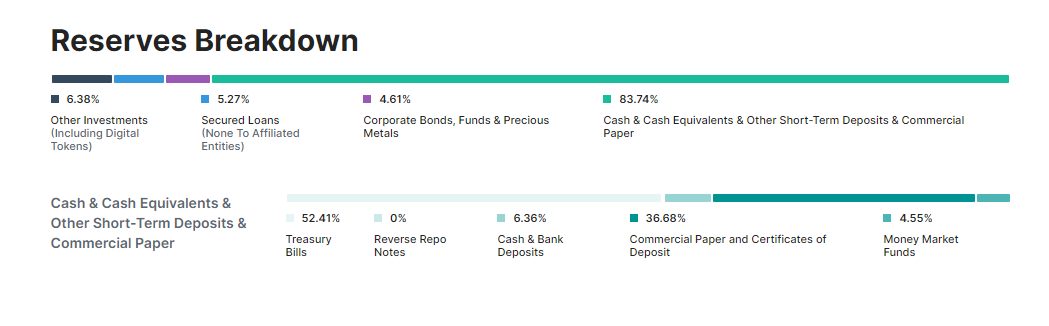

Centralized entities do not usually hold one-to-one the reserve asset. Commonly, the issuing company such are Tether, Circle, or Paxos, hold “cash equivalents” and debt of some kind from public and private institutions.

Figure 1. Tether reserves breakdown.

In addition, some of these entities refuse to be audited, emitting only attestations. This lack of transparency has generated rumors that some centralized stablecoins issuers do not have the reserves they claim to have. To throw more fuel into the fire, some do not even guarantee the redemption of the tokens for the assets that they are backing.

A Decentralized Stablecoin Challenge

Creating a functional decentralized, non-custodial stablecoin is inherently more complicated than digitizing fiat by issuing collateral-backed stablecoins.

The benefits include all the features crucial to traditional cryptocurrencies like Bitcoin: transparency, public access, censorship resistance, easy cross-border payment, no middleman and additional cost, and network resilience without single points of failure.

The challenges of decentralized stablecoins are equally plentiful:

- transparency (not great for commerce or privacy),

- lack of regulation vs. local laws and taxing

- high barriers to entry (self-custody and usage of non-custodial wallets and private keys)

- difficulty in creating stable pegs (it requires either collateralization of the stablecoin using real-world assets, which tend to be centralized or algorithms and digital assets, that as we saw on the example of Terra, may be attacked or/and unreliable)

- difficulty linking real-world collateral to autonomous digital on-chain protocols (perhaps, the new proof of reserve will help with that)

Some analysts claim that fully functional and useful decentralized stablecoin are impossible to make due to a problem called the Stablecoin trilemma. Inspired by the blockchain trilemma, the challenge of the Stablecoin trilemma is to create a stablecoin that is at the same time: decentralized, stable, and capital efficient.

- Decentralized: meaning that there is not a centralized entity minting the stablecoin tokens.

- Stable: meaning that it is able to maintain its peg, even in volatile market conditions.

- Capital efficient: meaning it needs minimum over-collateralization to maintain its peg.

All currently available stablecoins can achieve only 2 out of those 3 features, which is why it's called a Stablecoin trilemma.

The Stablecoin Trilemma

— ChainLinkGod.eth (@ChainLinkGod) May 24, 2022

You can choose two of three

1. Price Stability

2. Decentralization

3. Capital Efficiency

The ultimate goal is figuring out how to achieve all three simultaneously (at scale) https://t.co/yRFXZrDBit pic.twitter.com/yHyASvMj2M

What Nuon brings to the table

Nuon is a decentralized family of inflation-proof stablecoins, meaning that you don’t have to trust anyone, plus its smart contracts are audited by multiple renowned security companies in the space.

Unlike other stablecoin out there, Nuon is also inflation-proof, so the peg will be adjusted according to inflation data. But of course, not any type of data suffices. Nuon uses Truflation’s Chainlink oracles to gauge the daily levels of inflation. That means that it's up-to-date data, as well as reliable and verifiable, as it resides on the blockchain.

But what about the “death spiral,” you may ask? Nuon is immune to it because it is fully collateralized and backed by a basket of assets, Bitcoin and Ether (among others). It also contains algorithms that make sure Nuon coins are backed at all times despite market movements. Read more about how it works in Nuon's whitepaper.

So what Nuon really brings to the table is peace of mind. Investors can “park” their money into a Nuon family stablecoin without worrying that its value will be washed up by inflation, safe from centralized entities and middlemen that can freeze withdrawals or refuse redemption, and finally, secured from de-pegging by the complete collateralization.

Learn more about Nuon Finance and join our communities.

Written by ZestyBlockchain

Edited by Natalia Nowakowska